Many people don’t fully understand the basics of homeowners insurance. Many of us dread the thought of making another financial decision. And yet procrastination is not an option in this case because for most of us, our home is our biggest asset.

If you are unlucky and disaster strikes, you want to have enough insurance coverage to rebuild the structure of your home. You also want to be able to replace your possessions, cover costs if you can’t live in your home and protect you from the risk of liability.

To make a decision on adequate insurance coverage for your home, you will have to evaluate your specific risks of various hazards that could affect you and your house. In this blog post, I will assess my risks and decide on the insurance coverage for our home.

Disclaimer: I am not a financial professional. Everything on this Website represents my personal opinions or the personal opinions of others and should not be construed as financial advice. Please talk to a professional if you need specific financial advice.

Why I Forgot to Buy Insurance For Our Home

We closed on our new home on April 17th, 2020, and as of May 6th, we still didn’t have insurance on our house.

Why?

Typically this doesn’t happen because before you close on a home, the lender requires evidence of insurance. But we don’t have a loan this time, so no one reminded me to buy home insurance. I think I got too excited about planning for our new deck and forgot about insurance coverage.

Bad excuse!

My wife and I have worked hard for 30 years in Southern California. After many years, we were able to buy a condo in Los Angeles, which we sold, then bought a house in Pasadena, which we sold to buy this house in Delaware.

In case you don’t know, house prices in Delaware are significantly lower than in Southern California. As a comparison, the house we bought in Lewes is bigger than the one we had in Pasadena, but it cost almost 3-times less. This was a big decision for our early retirement.

But I digress. I have no excuse to have forgotten to insure our new house. One of the many important things to do before moving into your new house.

I better to take care of it now, before something happens.

The Basics of Homeowners Insurance

Why do we need homeowners insurance anyhow? I think I have a general understanding, but I’d like to know more before I choose a quote from an insurance company.

I came across this informative video from the Insurance Information Institute that goes over the fundamentals of homeowners’ insurance.

What Homeowners Insurance Policy Do I Need?

The HO-3 is the most common home insurance policy type. It offers a wide range of coverage for your home and other structures as an open-perils basis, which means it can cover any risks except for those specifically excluded in the policy. Coverage for personal property is handled on a named-perils basis, which means only events listed in the policy will be paid by the insurer.

Do not confuse homeowners insurance with home warranties.

A standard homeowners policy offers the following coverage:

- Dwelling (Often called coverage A) – Pays to rebuild or repair the physical structure of your home and attached structures, including mechanical and electrical systems. Commonly covered hazards in standard policy insurance are fire, hurricane, hail, lightning, and other disasters listed in your policy. A standard homeowners’ insurance typically doesn’t cover damage caused by earthquakes, floods, sewer backups, sinkholes, and acts of war.

- Other Structures (Often called coverage B) – Pays for damage to detached structures on your property. That is structures located on your property and not connected to your home.

- Personal Property (Often called coverage C) – Covers your personal belongings, including furniture, clothes, sports equipment, appliances, and other personal items if they’re stolen, damaged, or destroyed by insured disasters.

- Loss of Use (Often called coverage D) – Pays for additional living expenses if you need to live somewhere else due to a covered loss. This will not pay for all living expenses; it will pay for any additional living expenses, meaning any necessary expense that exceeds what you normally spend.

- Personal Liability (Often called coverage E) – Covers claims made or suits brought against an insured because of bodily injury or property damage.

- Medical Expense (Often called coverage F) – Covers claims made when someone is injured at your home regardless of who is at fault.

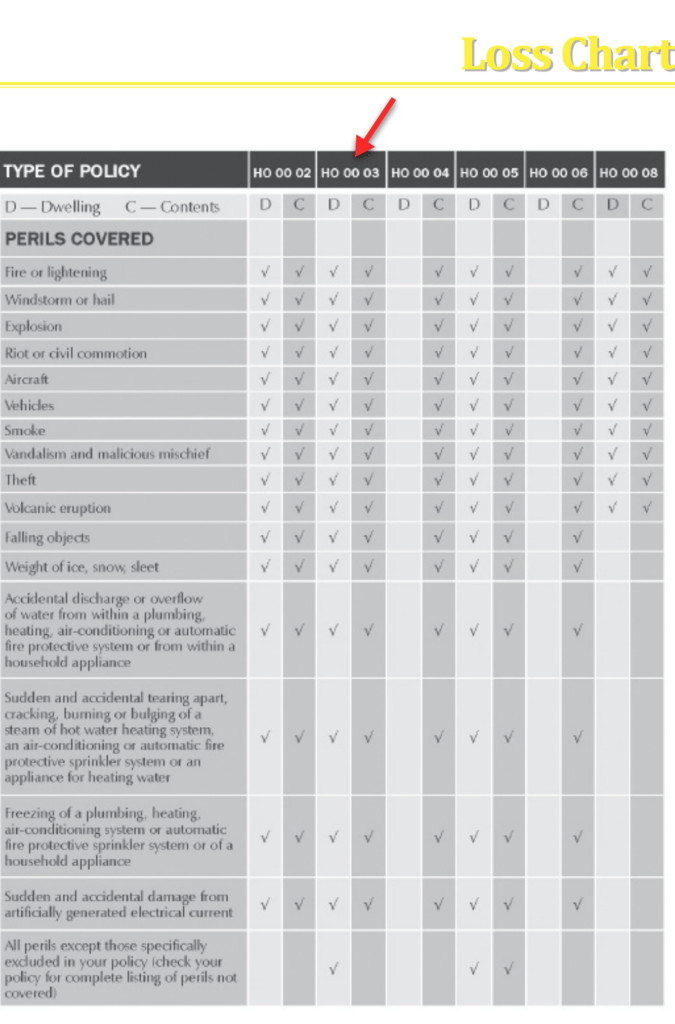

Below is a Loss Chart showing the perils covered for D-Dwelling and C-Contents for all home insurance policy types, including HO-3 (see the red arrow on the chart.) This chart is included in The Instant Insurance Guide: Home from the State of Delaware Department of Insurance.

Create a Home Inventory List

Coverage C of your homeowners’ insurance will show coverage for your personal property up to your limit. But how do you know what you had after a total loss?

If you are like me, you don’t want to go through all the items you possess and make an inventory list. United Policyholders, a non-profit organization helping consumers from all over the United States, convinced me to complete an inventory once we move to our new home.

Why do you need a home inventory list? United Policyholders explains why.

Because preparing an inventory after a total loss for insurance or taxes is very painful, difficult, and time-consuming. And, especially after a traumatic loss, it’s impossible to remember everything you had, so most people never collect their full insurance benefits.

They have this very detailed and handy Home Inventory List Spreadsheet (Excel) I am planning on using for our house inventory.

What Deductible Should I Choose?

A deductible is a specified amount of money that the insured is responsible for paying before the insurance company will pay a claim.

Typical minimum deductibles offered by insurers are $500 or $1,000 deductible. The Insurance Information Institute believes that you should take the highest deductible you can afford to save money on your premium.

Consideration of Insurance for Floods and Earthquakes

Standard homeowners’ policies don’t offer coverage for floods or earthquakes.

When you have a mortgage, the Federal Disaster Protection Act (FDPA) mandates that financial institutions ensure adequate coverage is in place for properties located in a flood zone.

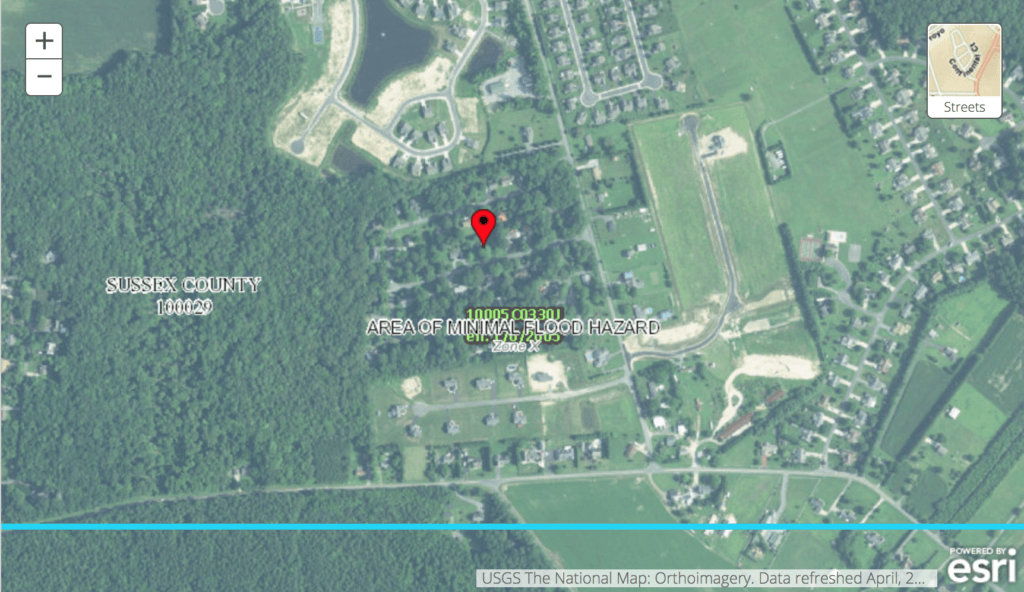

Since we don’t have a mortgage, I went to the FEMA Flood Map Service Center portal and search for my address to see if it is in a flood hazard area. It turns out it is in Zone X (area of minimal flood hazard). There is always a chance to be flooded, but the risk for our house is very low. So I will not insure our house for flood hazards.

What about earthquakes? Coming from Los Angeles, we know what earthquakes feel like. I will never forget the 1994 Northridge earthquake. My son was two years old at the time and was sleeping on his crib. We planned to take cover under the living room table in the event of an earthquake.

We followed our plan. The earthquake waked up most people in Southern California at 4:30 am. It felt so big, I thought it was the end. The jolts were so strong; I could barely get out of bed to pick up my son and get under the table. I injured my left heal walking over falling objects in our living room, but we felt blessed when it was all over.

Because earthquakes are so probable in Southern California, insurance coverage is very expensive, and deductibles are ridiculously high. But that’s another story.

We are now in Delaware. What is the risk of an earthquake in my area? According to The Delaware Geological Survey, the largest recorded event in Delaware occurred in 1973 and had an estimated magnitude of 3.8, which is a small earthquake. That means we don’t need earthquake insurance either.

Coverage and Quotes We Received for Our House

I was a little bit in a rush since I forgot to get insurance when we close on the house three weeks ago, which is a big unnecessary risk we can’t afford and it was my fault. Since I don’t have a lot of time to search for many insurance companies, I want to get the house covered fast.

I received these three quotes I am listing below.

| Coverage Type | AAA | Progressive | Travellers |

| A. Dwelling | $400,000 | $400,000 | $400,000 |

| B. Other Structures | $40,000 | $40,000 | $40,000 |

| C. Personal Property | $280,000 | $200,000 | $200,000 |

| D. Loss of Use | $120,000 | $80,000 | $120,000 |

| E. Liability | $500,000 | $500,000 | $500,000 |

| F. Medical Payments | $10,000 | $5,000 | $5,000 |

| Deductible (for hurricanes) | $20,000 | $500 | $1,000 |

| Deductible (all other perils) | $1,000 | $500 | $1,000 |

| Annual Premium | $777 | $777 | $1,227 |

Let’s go over what I received.

Dwelling coverage: I decided a $400,000 dwelling coverage will be sufficient to rebuild the whole house. That’s what is recommended by most insurance experts. The simple rule to determine if you have adequate insurance coverage is in the event of a total loss, you should have enough coverage to replace your belongings.

An important thing to keep in mind at time goes by is that typically house prices rise and fall, but the cost of building materials and labor always goes up.

Travellers’ quote is the highest: Right off the bat, we can see the quote from Travellers is 58% higher than Progressive and AAA. So I already think that Travellers is not my best option out of the three.

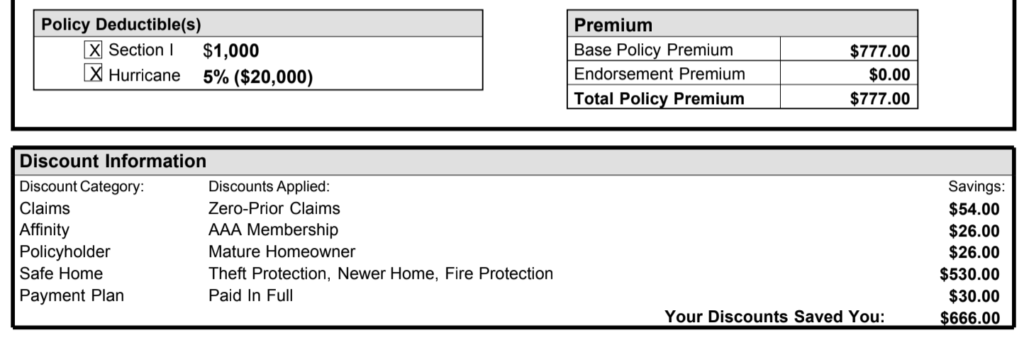

Identical quotes: Notice that the quotes I received for AAA and Progressive are identical. I don’t think this is a coincidence. I was dealing with an insurance agent from AAA Mid-Atlantic, which was able to also provide quotes from other insurance companies.

After the following AAA discounts totaling $666, the annual premium came out to $777, the same quote as Progressive. I think she just adjusted it until it became the same quote.

Other Structures Coverage: I tried to save money by removing the Other Structures coverage. I currently don’t have other structures, such as a pool, fence, greenhouse, shed, etc.

She mentioned that I couldn’t remove it because it had to be applied by law at 10% of the listed value of the home. I did a quick search, and that seems to be accurate, and apparently, it wouldn’t change the premium amount, even if I could remove it.

Personal Property Coverage: AAA would pay $80,000 more than Progressive to replace personal property items. This is where the home inventory list mentioned above will come handy. But to be honest, we don’t have close to $280,000 worth in personal property. So, I think $200,000 would be more than sufficient for us. But it doesn’t hurt.

Loss of Use Coverage: AAA is also better than Progressive here. It would pay $40,000 in living expenses if we have to abandon our home temporarily due to a covered hazard. I can’t imagine a situation where we would need to spend $120,000 while we are living somewhere else. But it doesn’t hurt either.

Liability Coverage: The three companies offer the same coverage of $500,000.

Medical Payments: AAA again offers a better deal here, paying a maximum of $10,000, which is $5,000 more than Progressive.

Deductible: AAA here is worse than Progressive. We would have to pay $1,000 for most perils before AAA pays us, which is $500 more than Progressive.

The item that is significantly different is the deductible for hurricanes. With AAA, we would have to pay $20,000 before they pay any amount if a hurricane causes the damage. With Progressive, the deductible is only $500.

I know earthquakes, but I’m new to hurricanes. What is the likelihood that my house gets damaged due to hurricanes in Delaware?

Hurricane Sandy’s impact in Delaware

The most recent significant hurricane that affected Delaware was Hurricane Sandy on October 29–30, 2012.

We live about Four miles from Rehoboth Bay and eight miles from the Rehoboth and Lewes beach. The beaches are one of the reasons we moved to Delaware. But when it comes to hurricanes, the closer you are to the beach, the worse it is. Thankfully, I don’t think we are dangerously close.

Hurricane can cause two major perils: wind damage and flood damage.

Flood is not covered by a standard home insurance, and I already determined above that my house is in a Zone X (area of minimal flood hazard). So, I will not get separate coverage for flood.

I think my risk is wind related damage, which is covered by the quotes I received, but AAA has a deductible of $20,000 compared to $500 with Progressive.

This video of Sandy’s impact in Delaware tells me that the risk is real. However, based on this list of hurricanes in Delaware from Wikipedia, in the last ten years, Sandy has been the hurricane with the most impact in Delaware and did not cause much damage inland.

Here comes decision time.

Why We Chose AAA

I think based on all the facts noted above, the most logical choice would probably be Progressive, and yet we chose AAA.

Why?

The most important reason is that we have no experience with Progressive and can’t tell how happy we would be dealing with them. We have had several claims in the past with AAA, which were resolved without any problems.

The conclusion is that we are getting a little better coverage with AAA for Personal Property, Loss of Use, and Medical Payments, but we are worse off if we have a hurricane-related claim.

Most experts recommend reassessing your policy and values annually. I will revisit our home insurance coverage in 1 year. I have added this item as a recurring todo to my house calendar.

Video Summary of Insurance Coverage

Let’s wrap up with a quick summary video I have created. If you like this video, consider subscribing to the House Notebook Youtube Channel. And thank you for your visit.

Related Posts: